Insurance is meant to provide financial security and peace of mind in times of need.

However, recent investigations and reports have revealed troubling practices within the insurance industry that undermine this fundamental promise.

One of the most concerning issues is insurance fraud, not only committed by policyholders but also by some insurance companies themselves.

On July 14, 2020, a revealing episode of the investigative program “Checkpoint” shed light on illegal deductions and unethical behaviors by well-known insurance companies.

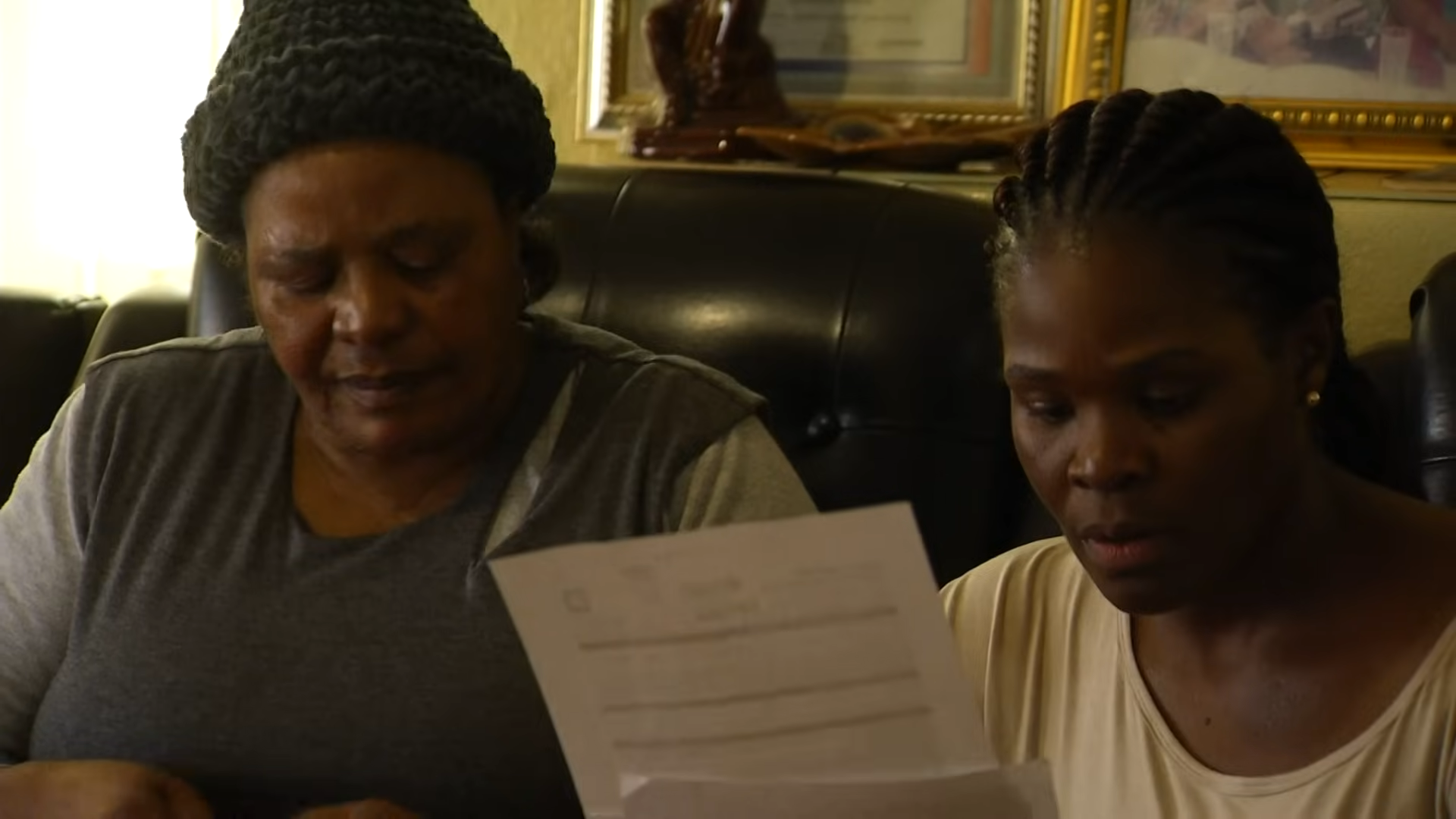

The report highlighted cases where government grant recipients were subjected to unauthorized deductions for funeral policies they never signed up for.

Additionally, it exposed another trusted insurer that faced severe criticism from the courts for canceling policies worth millions without proper justification.

These revelations have sparked outrage and concern among consumers, regulators, and advocates for fair business practices.

They point to systemic problems that require urgent attention and reform.

Insurance fraud traditionally refers to dishonest acts by policyholders who file false claims or exaggerate losses to receive undue benefits.

However, the scope of fraud extends beyond this narrow definition.

When insurance companies engage in deceptive or illegal practices, it not only harms individual clients but also erodes public trust in the entire industry.

The case of illegal deductions from government grant recipients is particularly egregious.

Many vulnerable individuals rely on government support to meet basic needs.

The unauthorized withdrawal of funds for funeral policies that were never agreed upon adds financial strain and emotional distress.

Such practices raise serious ethical and legal questions.

How can companies justify charging customers for products they did not consent to purchase?

What mechanisms are in place to protect consumers from such exploitation?

Regulatory bodies play a crucial role in monitoring and enforcing compliance within the insurance sector.

However, enforcement can be challenging due to the complexity of financial products and the resources required for thorough investigations.

Consumer awareness and vigilance are equally important.

Individuals must be encouraged to review their financial statements regularly and question any unfamiliar charges.

Access to clear information and transparent communication from insurers is essential to empower consumers.

The second issue highlighted in the “Checkpoint” report involved an insurer that canceled policies worth millions.

Policy cancellations can occur for legitimate reasons, such as non-payment of premiums or fraud by the policyholder.

However, when cancellations happen without proper cause or due process, they represent a breach of trust and contractual obligations.

The courts’ condemnation of this insurer underscores the seriousness of such misconduct.

Legal recourse is available to consumers who believe their policies have been unjustly canceled, but the process can be lengthy and costly.

This situation illustrates the power imbalance between large insurance companies and individual policyholders.

Consumers often lack the resources or knowledge to challenge unfair practices effectively.

Insurance companies must adhere to high standards of ethics and transparency.

Their business depends on public confidence, which can be easily damaged by reports of fraud or malpractice.

The financial impact of insurance fraud and unethical practices extends beyond individual victims.

It contributes to higher premiums for all customers as companies attempt to recoup losses.

It also burdens the judicial and regulatory systems with disputes and litigation.

Addressing these challenges requires a multi-faceted approach.

Stronger regulatory frameworks, enhanced oversight, and harsher penalties for violations are necessary.

Technology can also play a role in detecting and preventing fraud.

Advanced data analytics and artificial intelligence tools help identify suspicious patterns and flag potentially fraudulent activities.

Education campaigns are vital to inform consumers about their rights and the signs of insurance fraud.

Empowered consumers are less likely to fall victim to scams or unauthorized charges.

Industry associations and professional bodies should promote ethical standards and best practices among their members.

Self-regulation complements formal oversight and fosters a culture of integrity.

The cases revealed by “Checkpoint” serve as a wake-up call.

They remind us that vigilance is required not only against fraud by individuals but also against misconduct by corporations entrusted with safeguarding public interests.

Consumers affected by illegal deductions or wrongful policy cancellations deserve justice and compensation.

Their experiences should inform policy reforms and industry improvements.

Insurance companies must rebuild trust through accountability and transparency.

Open communication and responsive customer service are key components of this effort.

Government agencies should prioritize investigations into reported abuses and ensure swift action.

Collaboration between regulators, consumer groups, and the insurance industry can enhance effectiveness.

The media plays a critical role in exposing wrongdoing and raising public awareness.

Investigative journalism, like the “Checkpoint” episode, shines a light on hidden issues and pressures stakeholders to act.

In conclusion, insurance fraud and unethical practices by insurers pose significant risks to consumers and the broader financial system.

Illegal deductions and unjust policy cancellations are symptoms of deeper problems that demand comprehensive solutions.

Protecting consumers requires concerted efforts from regulators, industry players, and the public.

By fostering transparency, accountability, and education, we can work towards an insurance sector that truly serves its purpose.

As individuals, staying informed and vigilant is our first line of defense.

Review your policies carefully, ask questions, and report suspicious activities.

Together, we can help build a fairer, more trustworthy insurance industry that honors its commitments and supports those it serves in times of need.