The Programmable Promise – How DeFi and Smart Contracts are Rewriting the Rules of Trust

The Programmable Promise – How DeFi and Smart Contracts are Rewriting the Rules of Trust

For centuries, the financial world has operated on a “Human-in-the-Middle” model.

Whether you were buying a house, filing an insurance claim, or transferring money across borders, you were relying on a central intermediary—a bank, a broker, or an adjuster—to verify the truth and execute the contract.

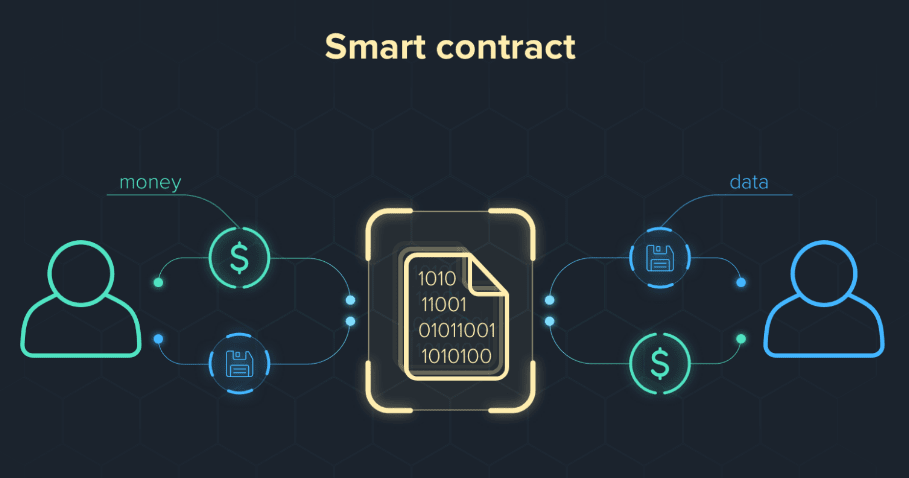

In 2026, this model is being challenged by a more efficient, math-based alternative: Decentralized Finance (DeFi) and Smart Contracts.

We are moving toward a “Programmable Economy,” where trust is not granted by a brand name, but by the immutable logic of code.

The Death of the Claims Process: Parametric Insurance

The most frustrating part of traditional insurance is the “Lag.” When a disaster strikes, you enter a weeks-long (or months-long) process of filing paperwork, waiting for an adjuster, and negotiating a settlement.

In 2026, Parametric Insurance powered by smart contracts is changing this.

Imagine a flight-delay policy or a crop-failure policy for a small farmer.

There is no “claims department.” The contract is connected to an “Oracle”—a verified data feed (like flight logs or satellite weather data).

If the data shows the flight was delayed more than two hours or that rainfall was below a certain threshold, the smart contract triggers automatically.

The funds are moved to your wallet in seconds.

This is “Trustless Insurance.” It removes the administrative overhead, eliminates the possibility of human bias, and provides liquidity exactly when it is needed most.

Liquidity as a Utility: The Rise of Real-World Assets (RWAs)

One of the biggest breakthroughs of 2026 is the Tokenization of Real-World Assets.

Historically, wealth was “locked up” in illiquid forms—your home equity, a piece of fine art, or a private business.

To access that value, you had to sell the asset or take out a complex loan.

DeFi protocols are now allowing these assets to be “on-chained.” By turning a property deed into a digital token, you can use a fraction of your home’s value as collateral to take out an instant, low-interest loan from a global liquidity pool, 24/7, without a credit check from a local bank.

Your “net worth” is becoming liquid and “programmable,” allowing you to move capital with the speed of an email.

The Concentration of Risk: The “Protocol Failure” Factor

However, moving from human systems to code-based systems introduces a new type of vulnerability: Smart Contract Risk.

In 2026, we’ve seen that while a blockchain is hard to “hack,” the logic within a specific contract can have flaws.

A bug in the code can lead to a “drain” of funds that is irreversible.

Unlike a bank, there is no “Reversal” button in a decentralized protocol.

This has given birth to a new industry: DeFi Protocol Insurance.

Sophisticated investors in 2026 don’t just “yield farm”; they buy coverage against “technical failure” or “governance attacks.” We are seeing the traditional insurance industry and the crypto world merge, as legacy insurers begin to underwrite the code itself.

Disintermediation: Becoming Your Own Bank

The core philosophy of DeFi is “Sovereignty.” It allows you to bypass the “gatekeepers” who take a 3% to 5% cut of every transaction.

By participating in decentralized lending and borrowing, you are earning the “spread” that used to go to the bank’s headquarters and shareholders.

But being your own bank comes with a “Responsibility Tax.” There is no customer service line to call if you lose your private keys or send funds to the wrong address.

Financial literacy in 2026 now includes “Digital Custody”—understanding how to secure your assets using multi-signature wallets and cold storage.

If you want the freedom of the code, you must accept the finality of the ledger.

-p-1080.png)

The Regulatory Frontier: From “Wild West” to “Compliance Pro”

As of 2026, the era of the “unregulated” DeFi is ending.

Governments are introducing frameworks that require decentralized protocols to integrate “identity layers” (Know Your Customer – KYC) without sacrificing privacy.

This is actually a “Bullish” sign for the average person.

As DeFi becomes compliant, it allows institutional capital—pension funds and large insurers—to enter the space.

This stabilizes the volatility and brings the “best of both worlds”: the efficiency of the blockchain with the consumer protections of the traditional system.

Conclusion: The Logic of Abundance

The shift to programmable finance is not just a technological upgrade; it is a shift from Scarcity to Efficiency.

By removing the friction of human intermediaries, we lower the cost of capital for everyone.

To be a “Writer’s Style” investor in 2026 is to be a bridge-builder.

You keep your “bedrock” in the traditional world of regulated insurance and banking, but you use the “pipes” of DeFi to move, grow, and protect your wealth with unprecedented speed.

The future of money is not a place; it is a set of rules that execute themselves perfectly, every time.