The Psychology of Scarcity – Why Our Brains Struggle with Long-Term Wealth

The Psychology of Scarcity – Why Our Brains Struggle with Long-Term Wealth

Financial success is often marketed as a game of math—a series of calculations involving interest rates, tax brackets, and diversification.

However, for the average person, the struggle to build wealth has less to do with a lack of arithmetic and everything to do with the intricate, often flawed machinery of the human brain.

To master money, one must first master the “Psychology of Scarcity,” a mental state that distorts our perception of value, time, and risk.

The Tunnel Vision of “Not Enough”

Scarcity is not just a physical state of having little; it is a psychological phenomenon that “taxes” our cognitive load.

When we feel we are lacking something—whether it is time, money, or social connection—our brain enters a state of high-alert focus known as tunneling.

Imagine a pilot flying a plane through a storm.

If the fuel gauge is blinking red, the pilot stops worrying about the long-term flight path or the comfort of the passengers.

Their entire world narrows down to that blinking red light.

This “bandwidth tax” means we lose the ability to think ahead.

In financial terms, when we are worried about next week’s rent, our brain physically cannot process the importance of a retirement fund forty years away.

This is why many people trapped in cycles of debt make choices that seem “irrational” to outsiders; they aren’t being foolish, they are simply tunneling.

![]()

The Present Bias and the Dopamine Trap

One of the greatest hurdles in financial planning is Hyperbolic Discounting, or “Present Bias.” Evolutionarily, humans were rewarded for consuming resources immediately.

A calorie consumed today was a guarantee of survival; a calorie saved for next month was a risk.

In the modern world, this translates into the “instant gratification” loop.

The dopamine hit from a new purchase is immediate and visceral.

Conversely, the satisfaction of seeing a balance grow in a 401(k) or a life insurance policy is abstract and distant.

Our brains are effectively fighting against a biological impulse to feast today, even if it means famine tomorrow.

To overcome this, we must stop relying on willpower and start designing systems—such as automated savings and “out-of-sight” accounts—that protect us from our own primitive urges.

The Emotional Weight of Loss Aversion

Psychologically, the pain of losing $1,000 is twice as intense as the joy of gaining $1,000.

This is known as Loss Aversion.

In the realm of investing and insurance, this bias can be paralyzing.

Loss aversion leads many to stay in “safe” assets like cash or low-interest savings accounts during their prime earning years, effectively losing wealth to inflation over time.

It also causes people to cancel insurance policies during a financial “squeeze,” viewing the premium as a loss rather than a protection against a much larger, catastrophic loss.

Understanding that our fear of loss is often disproportionate to reality is the first step toward rational asset allocation.

We must train ourselves to look at the “expected value” of our decisions rather than the emotional sting of a monthly expense.

Anchoring and the Comparison Game

In the digital age, scarcity is often manufactured through social comparison.

We “anchor” our expectations of what a successful life looks like based on the curated highlights of others.

This leads to Lifestyle Creep—the phenomenon where every increase in income is immediately met by an increase in spending to maintain a social “status.”

When we anchor our happiness to a specific car, a certain neighborhood, or a brand of clothing, we are perpetually living in a state of self-imposed scarcity.

No matter how much we earn, the “tunnel” remains because the goalpost is always moving.

True financial independence begins when we decouple our self-worth from our net worth and choose internal benchmarks for success.

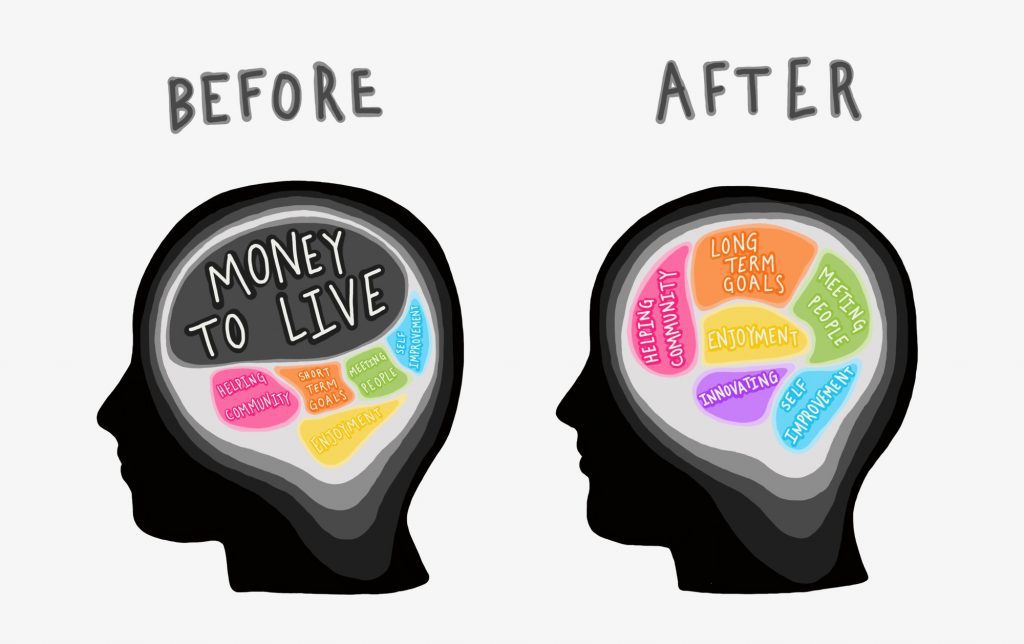

Reclaiming Your Cognitive Bandwidth

How do we break the cycle of scarcity and start thinking like long-term wealth builders?

- Slack and Buffers: In computing, “slack” is the space left in a system to prevent it from crashing.

- In finance, this is your emergency fund.

- Having three to six months of expenses isn’t just about the money; it’s about freeing up your brain’s “bandwidth” so you can stop tunneling and start planning.

- Pre-Commitment: Since we know our “future self” is more rational than our “current self,” we should make decisions in advance.

- Automating insurance premiums and investment contributions removes the emotional friction of the “choice.”

- Reframing Insurance: Instead of viewing insurance as an expense (a loss), reframe it as “pre-purchased peace.” It is the price of removing the worst-case scenario from your mental “tunnel,” allowing you to focus on growth.

The Wealthy Mindset

Wealth is not the absence of desire, but the presence of control.

By understanding the psychology of scarcity, we can recognize when our brains are trying to trick us into short-term thinking.

We learn to ignore the blinking red lights of consumerism and focus on the long-term horizon.

The most valuable asset you have is not your bank balance—it is your attention.

When you secure your foundation through sound insurance and consistent saving, you buy back your mental freedom.

You move from a life of reacting to a life of creating.